This article has been updated for new 2023 Rule H1 changes.

Summary: Pre-authorized debit forms are required to process PAD payments in Canada. There are also some requirements outlined by Payments Canada that must be present on a pre-authorized debit, including contact details, timing, amount, cancellation details, and more. PAD forms can be submitted in-person, or online, but there are stricter requirements if submitting online. There are also different requirements for notifying your customers of changes, depending on whether the payment amount was variable or fixed. Finally, the article includes some examples of filled-out pre-authorized debit forms, and includes a link to Rotessa’s PAD form generator, where you can generate compliant PAD forms online for free.

If you’re brand new to pre-authorized debit (PAD) processing, you might not be aware of how the authorization part works. No problem, we’ll walk you through everything you need to know. Here’s what you can expect in this article about PAD authorization forms (also known as PAD agreements):

What is a pre-authorized debit?

Pre-Authorized Debit, or PAD, is an electronic payment method that allows your business to withdraw money directly from your customer’s bank account. The term “pre-authorized” refers to an agreement between your business and your customer. In the agreement, the customer gives permission for you to withdraw money from their account based on the terms outlined. This can work for recurring payments on a set schedule, or variable amounts too.

To learn more, read our overview of pre-authorized debit payments.

Because pre-authorized debits are called many different names, it’s important to remember that PAD processing in Canada is the same as direct debit, automatic withdrawals and pre-authorized payments.

If you’re new to pre-authorized debits and want to learn the basics, here’s a beginner’s guide to help you through.

Now that we have taken care of the basics of PAD, let’s dig into what an authorization form is and why it’s an important part of the PAD process.

If you want to accept pre-authorized debits from your customers, you are legally required to receive authorization and document it. The entire point of a pre-authorized debit agreement is to make sure the payor (your customer) and the payee (your business) are on the same page. So when you withdraw money from their bank account, there are no surprises.

Payments Canada is the governing body that outlines and regulates the rules of pre-authorized debits in Canada. Rule H1 is a document that outlines every requirement. Because Rule H1 is a very long, technical guide, we’ve made a condensed list of requirements for pre-authorized debit authorization and the acceptable formats.

Mandatory requirements of a pre-authorized debit form

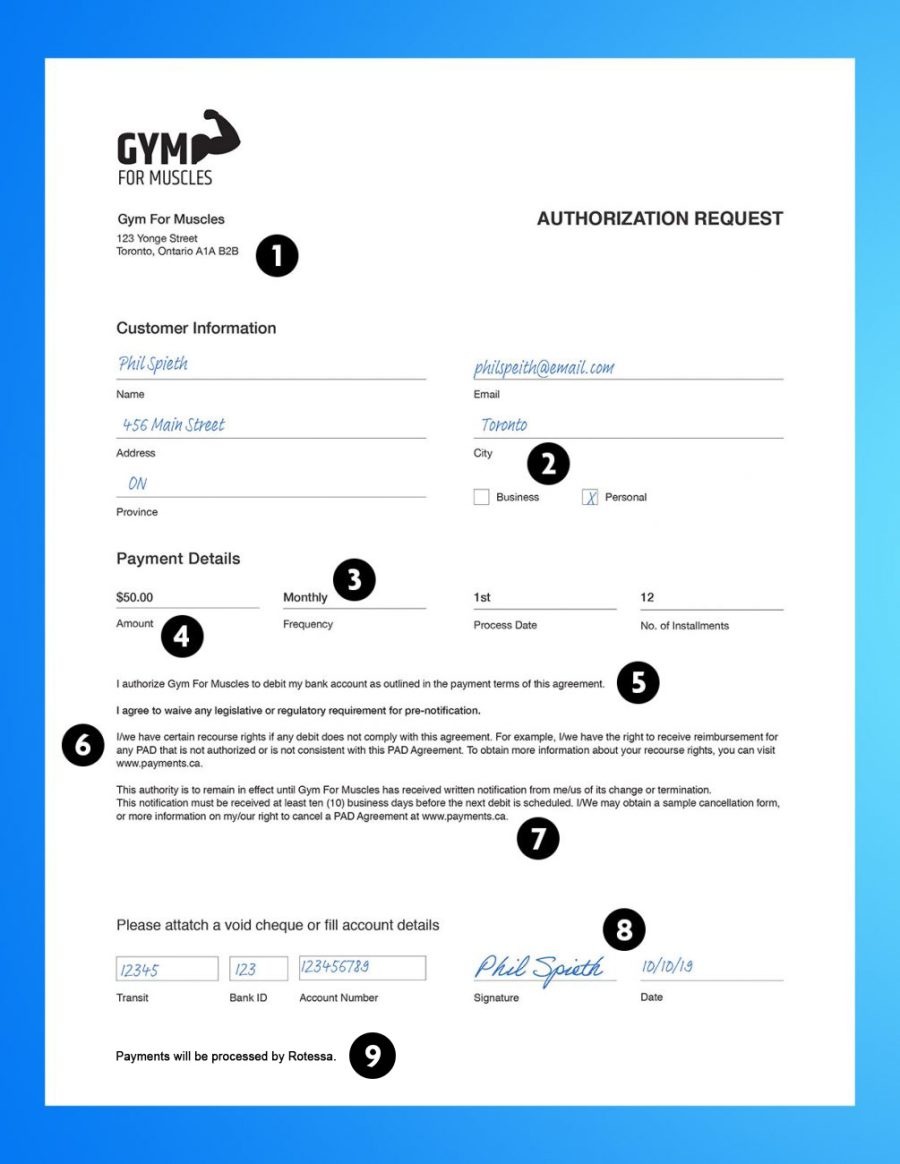

This is a what a PAD agreement form looks like, along with the required elements as outlined by Payments Canada:

If you follow along with the number guides, here’s an explanation of the eight requirements of a PAD form.

![]() Contact details – So the payor can get in touch with you.

Contact details – So the payor can get in touch with you.

![]() PAD category – Is the payor a person or a business?

PAD category – Is the payor a person or a business?

![]() Timing – This outlines to the payor when the payments are to be taken out (weekly, monthly, bi-monthly, annual, on set dates or otherwise.) You also need to explain if each payment is to be triggered by a specified act, event or other criteria. If it’s to be triggered by a specific act, it needs to be clear on what that is.

Timing – This outlines to the payor when the payments are to be taken out (weekly, monthly, bi-monthly, annual, on set dates or otherwise.) You also need to explain if each payment is to be triggered by a specified act, event or other criteria. If it’s to be triggered by a specific act, it needs to be clear on what that is.

![]() Amount – So the payor knows how much is being taken from their account. If it’s an authorization for variable amounts, it needs to be clearly stated.

Amount – So the payor knows how much is being taken from their account. If it’s an authorization for variable amounts, it needs to be clearly stated.

![]() Authorization statement – A clear statement that outlines authorization to withdraw funds from a particular account.

Authorization statement – A clear statement that outlines authorization to withdraw funds from a particular account.

![]() Recourse statement – So the payor understands their rights to reimbursement for unauthorized debits.

Recourse statement – So the payor understands their rights to reimbursement for unauthorized debits.

![]() Cancelation details – So the payor knows how to cancel the agreement.

Cancelation details – So the payor knows how to cancel the agreement.

![]() Date of agreement & signature (if a physical paper form).

Date of agreement & signature (if a physical paper form).

![]()

Pre-authorized debit form notification requirements

Payments Canada is very specific about the lead time required for you to notify your customers when the payments are coming out (remember; the point of PAD authorization is to have no payment surprises). Notification requirements depend on the type of agreement you have in place. Or, if specified, the payor and payee can mutually agree to waive or shorten the notification period.

For variable amounts

With variable amounts, you must give notice of the amount at least ten days notice before the payment is processed (unless both parties mutually agree to waive this period). You must also give notice if the payor asks you to change the amount.

For fixed amounts

You are required to give at least ten days’ notice before the first recurring withdrawal, which outlines the amount and payment schedule. No further notifications are required, assuming the amounts are never larger than the agreed-upon amount.

If included in the PAD agreement, the payor and payee can mutually agree to waive or shorten the notification period.

Pre-authorized debit form examples

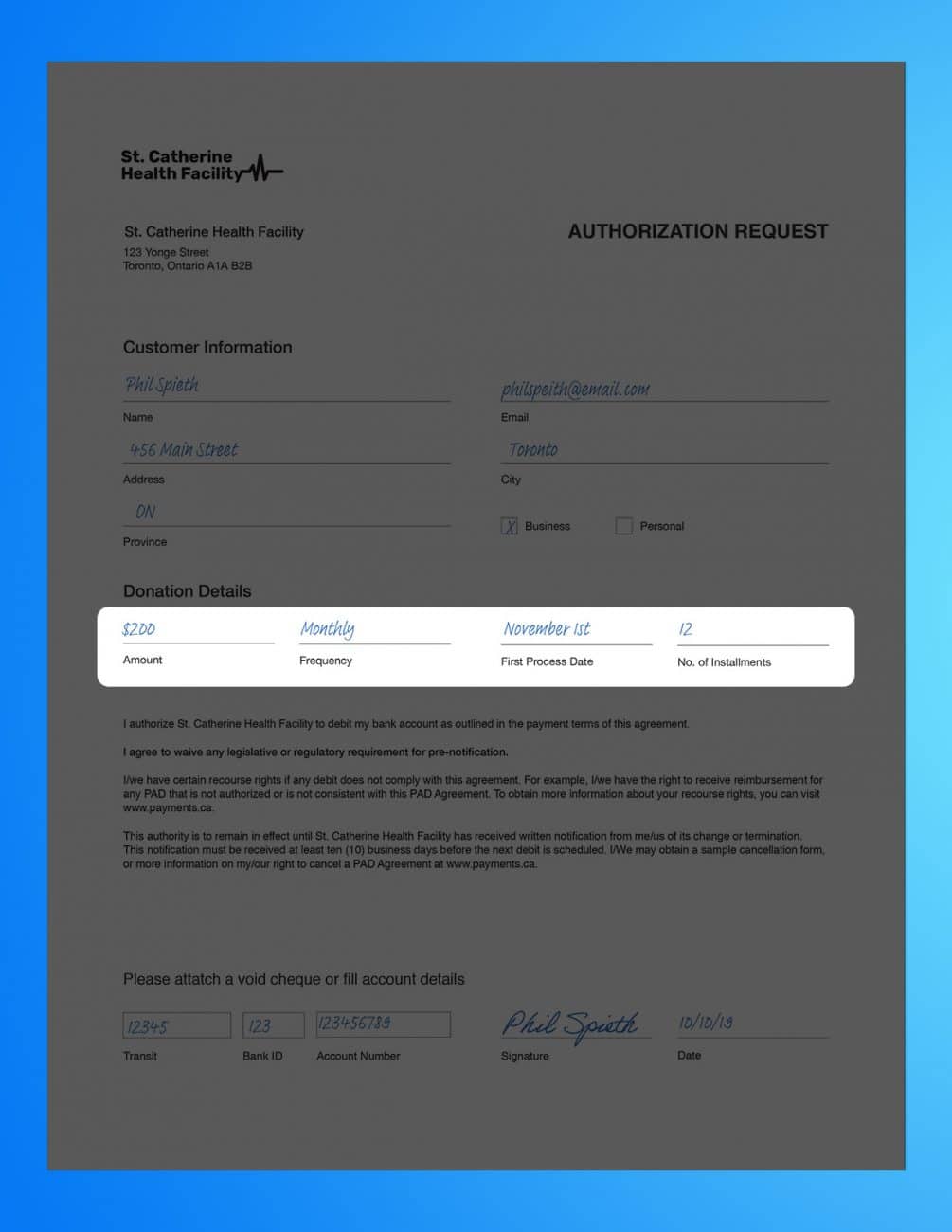

Payor-defined pre-authorized debit form

Industry Examples: Non-profit organizations or churches for donations.

Key Difference: In a payor-defined PAD form, the payor outlines the specific amount and timing of the payments.

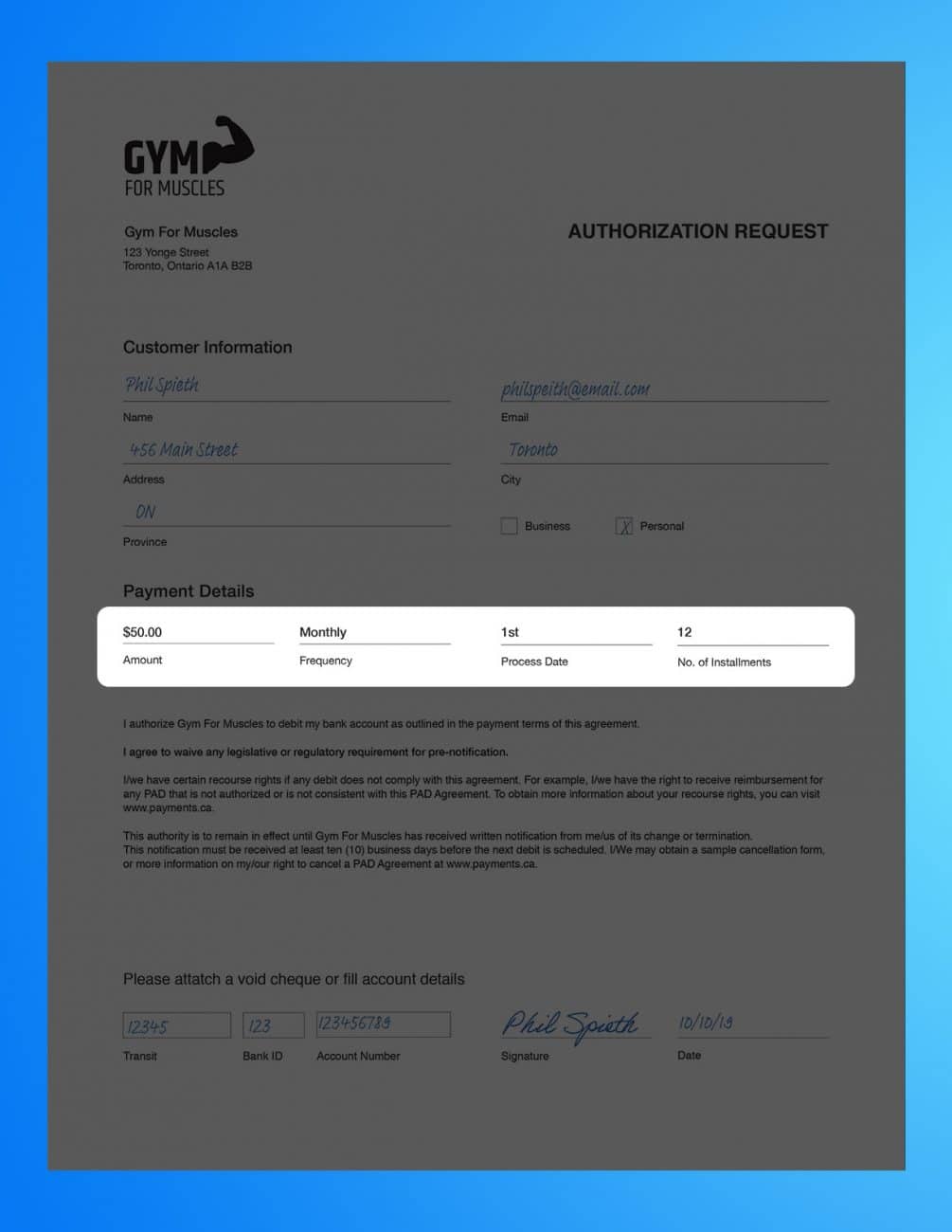

Fixed pre-authorized debit form

Industry Examples: Fitness centers, daycares, clubs and leagues for membership fees.

Key Difference: The payee outlines a specific fixed amount and timing schedule of the payments

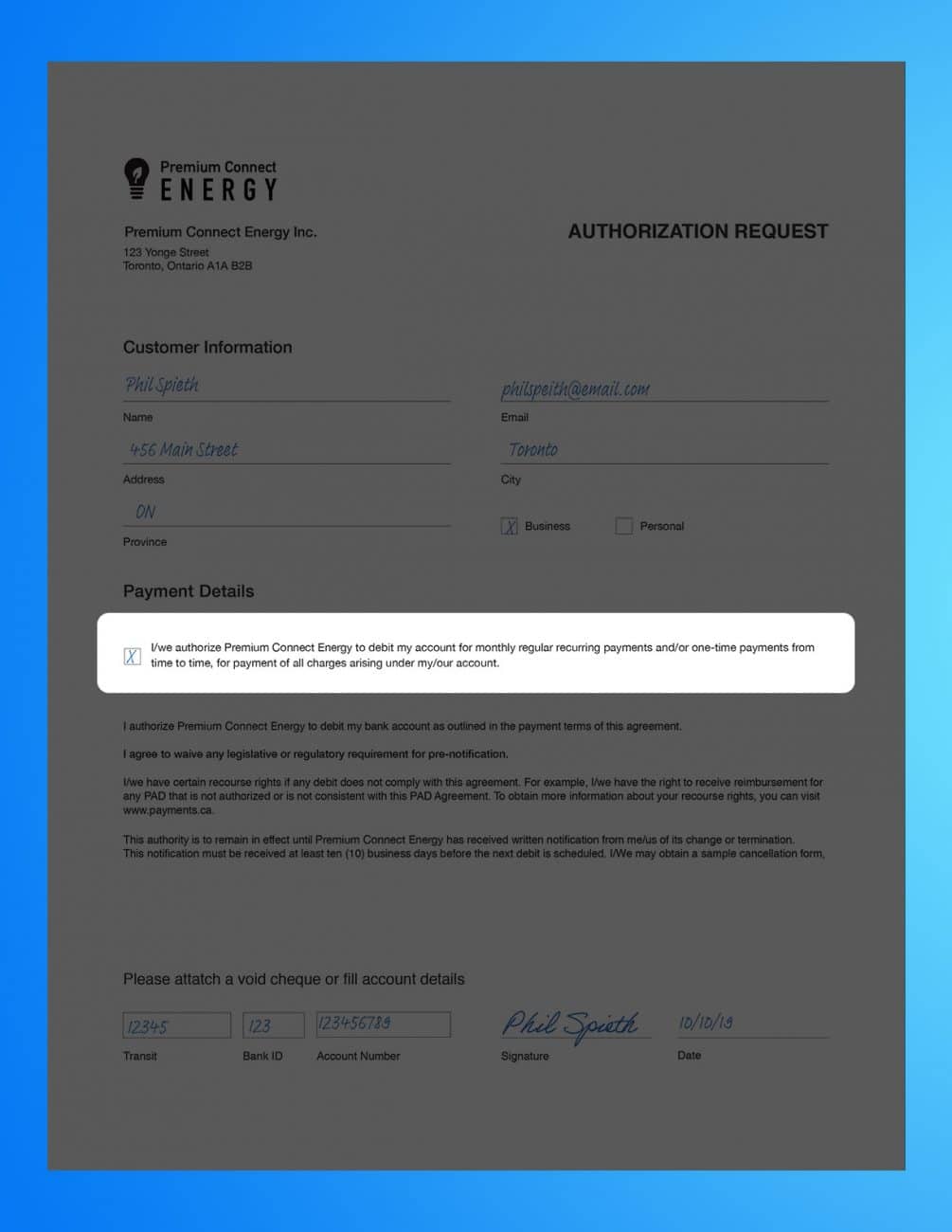

Variable pre-authorized debit form

Industry Examples: Utility company for usage or accountant, law office or marketing agency.

Key Difference: The payor agrees to allow the payee to debit their account on the schedule agreed to or based on the events outlined in the agreement.

Congrats! You now have all the tools and information to go out and build your own PAD Form!

There are no rules on how you must build a PAD form it or how it should look. As long as you have the necessary requirements, you can make it on your own. That being said…

FREE BONUS

We’ve built an online tool that makes it really easy to build your own pre-authorized debit forms. The PAD form generator lets you customize a PAD form with your logo, text and fields you want to include.

Share this content with a friend:

A better way to get paid

Withdraw money directly from your customer’s bank account when their payments are due. Schedule one-time or recurring payments to get paid on time.