Accountant & Bookkeeping Partner: Horizon CPA

Despite serving a large geographic area, Shane and Blaine of Horizon CPA have an outstanding reputation amongst their diverse clientele. Their "holistic" approach to their clients' finances has played a key role in their organic growth year after year.

Shane Wagstaff, founder of Horizon CPA, says their well-rounded view of a financial plan is what sets this practice apart and gives his clients the best start in their businesses. Shane, operating out of the Red Deer and Trochu locations, works with farmers, ranchers, oilfield contractors, holding companies and other small to mid-sized business clients. The relationships Shane has built and maintained with his hometown clients have helped his young practice grow steadily throughout the years. Words of mouth referrals are their greatest growth vertical and attest to the quality of work and care Horizon CPA provides.

Blaine Gendre joined the practice in early 2019. As an Albertan as well, Blaine came to the practice with experience in the oil, gas, and mining industries. Blaine services the firm's Edmonton client base and works alongside the business owners in that area to grow a well-rounded and successful business.

Horizon's clients, covering hundreds of kilometres of Alberta, are mostly rural, hard-working, and well-established. Shane and Blaine work with them to utilize cloud technology to manage their businesses finances. Since their launch, they have begun working for an increasing number of remote clients.

Therefore, by leveraging technology such as Microsoft Teams to meet with clients they have been able to increase not only the number of clients but also the number of kilometres between them. "70 percent of my clients I work with remotely as they are located over 2 hours away," says Blaine. By adopting this tech, their clients are able to focus more on what they love: their business.

In addition to their paid services, Horizon also offers great resources on their blog for Albertan business owners about budgeting, payroll, incorporation, and more.

As a new member of the Accountant and Bookkeeper Partner Program, Horizon is excited to start introducing Rotessa and Pre-authorized debits to their clients. In addition to their 30% transaction discount that they can share with clients and friends, they will also share their experience and business tips with us!

Simplify your payment process with Rotessa and Hawkins & Co

At Hawkins & Co. when we review software for clients, we look at key criteria to assess them against. Many criteria on the list are client-specific but there are a few that we consider on every software review we do. The top 3 criteria we always focus on are:

- User Interface - is it easy to use? How does it look when you log in? How many clicks does it take to get to what you’re looking for?

- Simplification - does it simplify a client’s process? Does it simplify the client’s interaction with their customers?

- Integrations - what does it integrate with? How does that integration work? Does the integration work consistently?

When we select software to use ourselves, we run through the same type of list. Over 5 years ago, when H & Co. was in its early years, we adopted Rotessa as the main payment option for our clients. We needed a system that was easy for collecting monthly payments from our clients. Even then Rotessa hit the mark. Five years later and Rotessa continues to meet our needs and function well - in tech years that’s a long time!

Now Rotessa’s even better - let’s rate Rotessa on our top 3 criteria then and now:

| Key Aspect | 5 years ago | Today |

| User Interface | 5 years ago

|

Today It’s been refreshed but still carries through the same consistent easy to use interface |

| Simplification | 5 years ago

|

Today Again it’s been refreshed and has allowed us to utilize a standard PAD request to our clients which makes it even simpler to roll out. Just one link and done! Matching has now been made even easier with a new Xero integration! |

| Integrations |

|

Today Now Rotessa integrates with Xero and we can set up our payments to automatically connect with Xero and match our clients invoicing. Making reconciliation a breeze! |

For Hawkins & Co., Rotessa has been a great solution that provides us with consistency and top-notch customer service. Our H & Co. payment process works well for our client payments but each business has different things to take into consideration.

So we wanted to invite Lissi Moffit, Communications Coordinator from Rotessa, to share other ways Rotessa can benefit your business:

At Rotessa, we are big fans of simple. We like to keep payments simple, reliable, and affordable.

Here’s an example of how most businesses get paid; As work gets done, or once the month is over, they send an invoice to their customers and wait for them to initiate a credit card payment or send in a cheque. The problem with this traditional payment process is:

You have no control over when you get paid. “Cash is king,” and everybody knows it. When you don’t have automatic payments set up, you are at the mercy of your customer and are probably waiting on them to pay you. Additionally, the true cost of credit cards is not small-business friendly. I understand that you want to give your customers every opportunity to pay you, but how much does this actually cost you? Most online credit card processors charge 2.9% on every payment.

If you invoice your client for $500 every month, that’s nearly $180 in fees a year for just one customer. Paying a flat rate per transaction, with automatic payments, gives you much better value and could literally save you hundreds (if not thousands) of dollars each month.

With Rotessa, you can integrate your payments with your account software and automatically schedule those bank payments with our feature Auto Sync. QuickBooks Online or Xero users who want to automate their workflow, simplify receivables, and get paid on time need Rotessa and Auto Sync.

We also give you the tools to manage multiple accounts all with one login. This feature is great for property managers, franchisees, daycare groups, bookkeepers, and anyone who is working with different accounts and businesses all in Rotessa.

Having the ability to collect payments easily, on a timely schedule, and with all the convenience of traditional digital payments, Rotessa and PADs help simplify your small business' payment process.

What are electronic funds transfers (EFT payments)? And how do I create one?

What is an EFT payment?

EFT stands for electronic funds transfer. An EFT payment is a bank to bank transfer initiated by a payee when the payor gives the authorization to do so.

These types of payments move money across a network, between banks, and frequently replace paper methods for making payments like cash or cheques.

You have probably sent or received EFT payments many times in your life, maybe without knowing it. Authorized your utilities or phone companies to automatically withdraw your monthly payments? That’s an EFT payment! Consumers, businesses, and government agencies use EFTs every day.

Pre-authorized debits and direct deposits are made possible by EFTs

Example path of an EFT payment

Step 1

Business invoices customer

Step 2

Business obtains customer's pre-authorized debit agreement

Step 3

Business initiates EFT payment from customer with third-party processing software

Step 4

Funds are transfered from customer's bank account and deposited into business'

Direct deposits are credits sent to a recipient's bank account. Often, paycheques and government benefits are deposited this way. These are all done with an EFT.

Pre-authorized debits (PADs) are payments withdrawn from a bank account. PADs are typically used to charge recurring payments like rent, donations, utilities and more.

Businesses can use EFTs in these ways to send or receive payments from suppliers or clients. Customers can pay businesses faster and more reliably by using an EFT payment options. Sounds great, doesn’t it? Later in this post, we’ll outline more benefits of accepting EFT transfers.

How do businesses get started with EFTs?

If you want to accept EFT payments from your customers, you are legally required to receive authorization (and document it). The Canadian Payments Association is the governing body that outlines and regulates the rules of EFT payments in Canada. It may seem complicated at first, but it’s simple. Your customer agrees to pay you with an electronic funds transfer, and you’re not waiting for another payment ever again!

How to create an EFT agreement and get paid

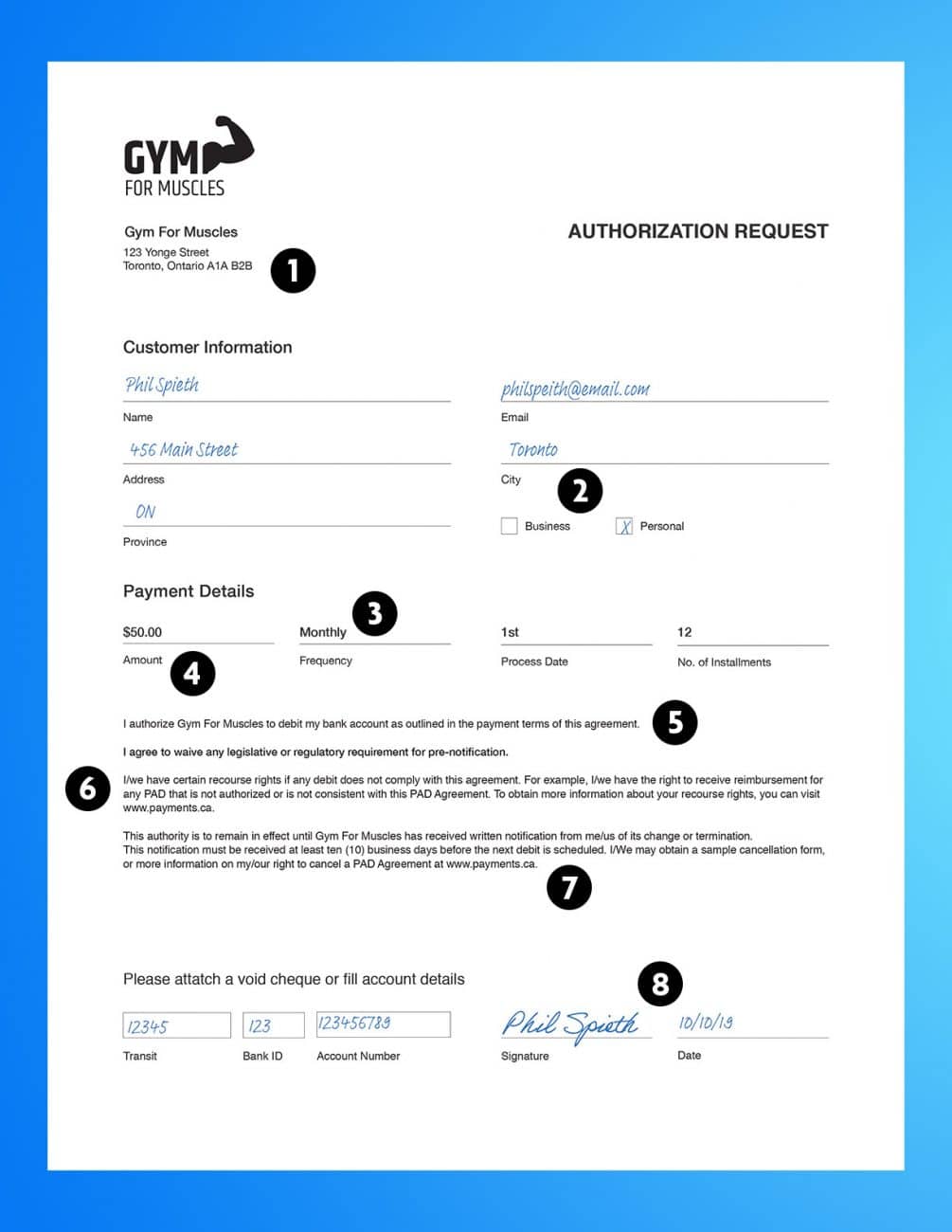

This is what an agreement looks like for an EFT payment:

If you follow along with the number guides, here’s an explanation of the 8 requirements of the EFT agreement.

![]() Contact Details - So the payor can get in touch with you.

Contact Details - So the payor can get in touch with you.

![]() Pre Authorized Debit Category - Is the payor a person or a business?

Pre Authorized Debit Category - Is the payor a person or a business?

![]() Timing - This outlines to the payor when the payments are to be taken out (i.e. weekly, monthly, bi-monthly, annual, on set dates or otherwise.) You also need to explain if each payment is to be triggered by a specified act, event or other criteria. If it’s to be triggered by a specific act, it needs to be clear on what that is.

Timing - This outlines to the payor when the payments are to be taken out (i.e. weekly, monthly, bi-monthly, annual, on set dates or otherwise.) You also need to explain if each payment is to be triggered by a specified act, event or other criteria. If it’s to be triggered by a specific act, it needs to be clear on what that is.

![]() Amount - So the payor knows how much is being taken from their account. If it’s an open or variable authorization, it needs to be clearly stated.

Amount - So the payor knows how much is being taken from their account. If it’s an open or variable authorization, it needs to be clearly stated.

![]() Authorization Statement - A clear statement that outlines authorization to withdraw funds from a particular account.

Authorization Statement - A clear statement that outlines authorization to withdraw funds from a particular account.

![]() Recourse Statement - So the payor understands their rights to stop the agreement.

Recourse Statement - So the payor understands their rights to stop the agreement.

![]() Cancelation Details - So the payor knows how to cancel the agreement.

Cancelation Details - So the payor knows how to cancel the agreement.

![]() Date of Agreement & Signature - If in a physical paper form

Date of Agreement & Signature - If in a physical paper form

The next step is to find a payment processor because, in order to withdraw money from your customers’ bank account, you will need to find a processor who can facilitate the payment. This is typically your bank or a third-party payment processor.

Finding a third party EFT processor

Unfortunately, bank systems are pretty complicated and do not integrate well with your accounting system. Third-party processors usually have integrations and give you a much more competitive rate for lower volume transactions. The user experience is also way friendlier.

At Rotessa, for example, we have a tool that creates an authorization form for your EFT payments. You can email customers with a unique and secure link that this tool provides.

Pre-authorized debit payments are simple and quick with Rotessa

Rotessa is your trusted partner for seamless payment automation and secure recurring payments. No onboarding costs or percentage-based fees.

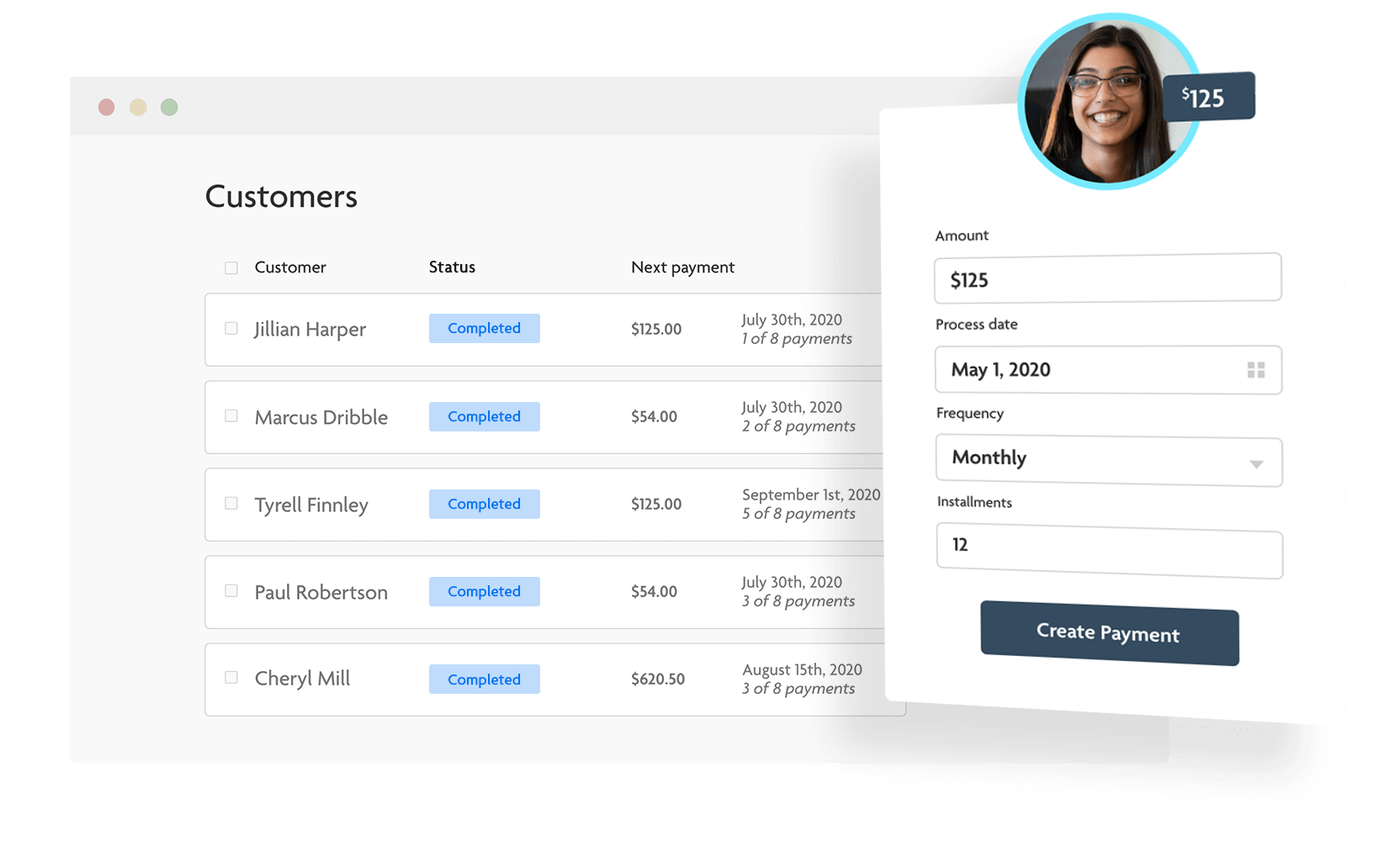

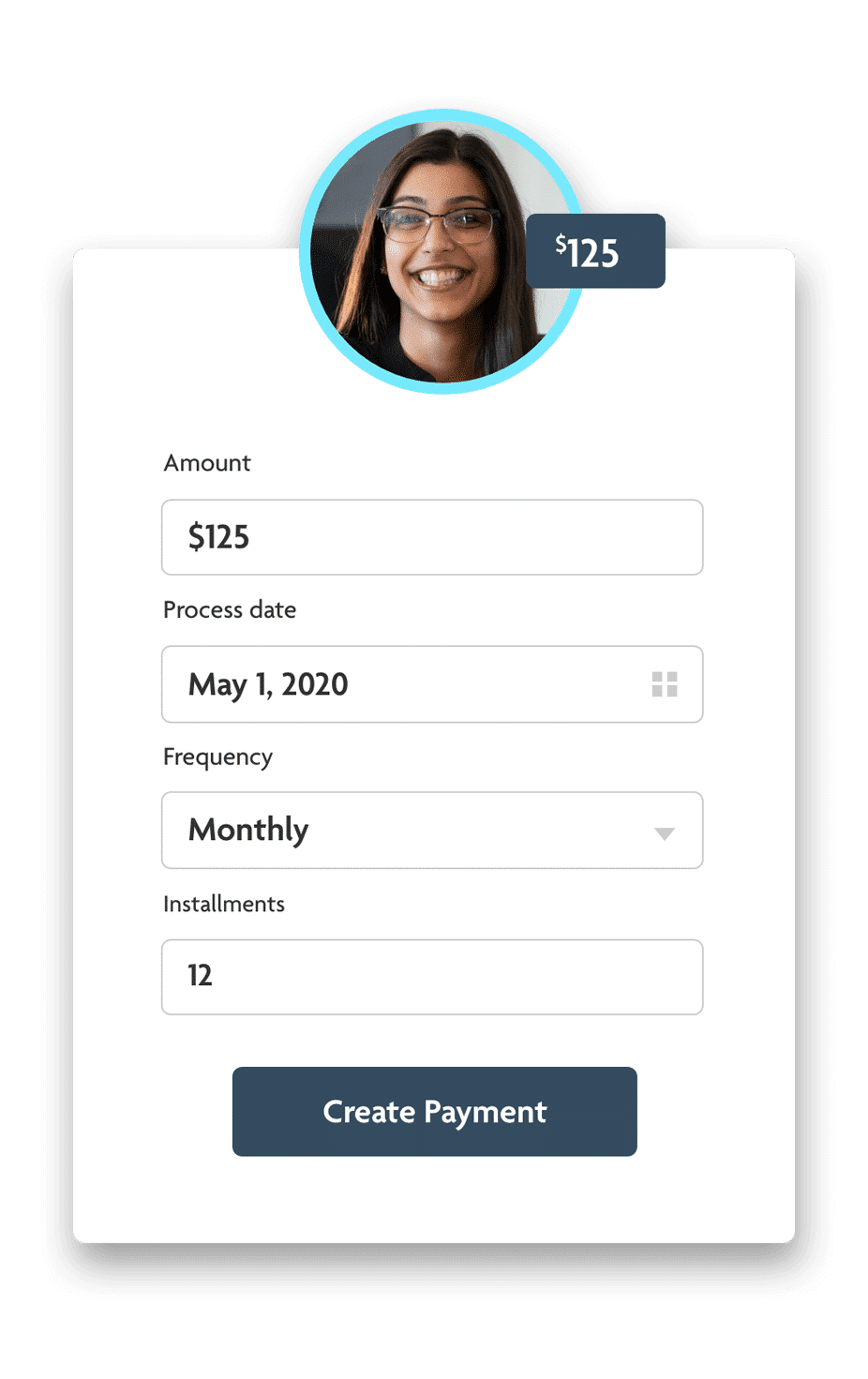

Setting up a payment

Once you've signed up with a processor you will get access to an online app. This app will allow you to set up and schedule payments from customers (once you get their EFT agreement). When setting up a payment, you need to outline the amount owing, the schedule and/or frequency of payments, and the number of installments.

Your EFT payments will now be automatically withdrawn from your customer’s account and deposited into yours according to the specified frequency and installment schedule.

With EFTs it is important that you remember that when you are scheduling payments, the processing date on your scheduled transaction is the day the money will be withdrawn from your customer’s account. With most processors, you will receive the settlement of funds a few business days later. Therefore, make sure to schedule accordingly.

On the settlement day, your payment processor will provide a settlement report of the EFT payments. With Rotessa, you get those reports for free and you can integrate them with your accounting software to reconcile those settled payments.

Four reasons to collect payments with EFTs

Reason 1: control

Most businesses receive payments by sending the customer an invoice and waiting for a credit card transaction or a cheque. This payment workflow can be a problem because it gives the customer the prerogative to initiate the payment. An EFT payment workflow, on the other hand, gives the prerogative to the business by allowing them to initiate payments from the customer.

As a business, you have no control over payments with credit cards and cheques. When you don’t have EFT payments set up, you are at the mercy of your customer and are probably waiting on them to pay you. You already provided your service, why should you allow your customers to choose when they pay for it? With EFT payments, you decide when payment is withdrawn from your customer’s bank account.

Reason 2: cost of credit cards

The true cost of credit cards is not beneficial to small businesses. Yes, you want to give your customers every opportunity to pay you, but how much does processing credit cards cost? Most online credit card processors charge 2.9% on every payment. So, if you invoice a client $500 you'll be paying almost $15 just to process one payment!

EFT processors don't charge a percentage fee (depending on which one you choose). With Rotessa, for example, that $500 invoice could cost as low as 30¢ to process! Businesses can save tens, hundreds or thousands of dollars every month with EFT payments.

Reason 3: timeline of cheques

Each time a customer sends you a cheque, you have to deposit it and reconcile it with your accounting platform. This is a time-consuming task that could be better spent on growing your business. With automatic EFT payments, you can schedule those payments in advance with no need to leave the office.

Reason 4: customer relationships

For many businesses, getting paid with other payment methods can create strained customer relationships. Not only is payment chasing frustrating, it can cause awkward confrontational interactions with customers. When a business and customer use an EFT they both agree on a processing date and an amount for the payment.

EFT payments give you the ability to collect payments easily, on a timely schedule, and with all the convenience of traditional digital payments. Want to give EFT payments a try? Simply set up a free Rotessa account!

Simplify Accounting and Rotessa

At Simplify Professional Corporation or Simplify Accounting, my firm is all about improving efficiencies and the customer experience with cloud-based technology.

Rotessa is one of the applications that my firm uses on a regular basis that does exactly that: it improves efficiencies in that customer experience. It's a payment solution provider. They use a pre-authorized debit to provide those payment solutions and they integrate with online accounting platforms like QuickBooks Online and Xero.

So how it works is you, essentially, send a link to your customer, they fill in their details, and then whenever you invoice them out of your accounting platforms like Xero or QuickBooks Online, then according to the payment terms of that invoice, you'll get paid when the invoice is due.

It's important to have a discussion with your customer, when they set up that payment process, that when you send that invoice that that's how it works so that they can ensure they have enough cash in the bank account to make that payment. You can work with them on payment terms if there's a cash flow crunch for them, but typically, they'll be able to pay you on those terms, depending on your customers.

It just makes it so much easier for both them as a customer and for your company.

You're not chasing down payments. They're not trying to figure out the best way to pay you. They're not calling you up with their credit card information. They're not sending you a check. It's just a really simple payment solution service.

The cool thing about Rotessa is that they're Canadian. They're based in Steinbach, Manitoba, Western Canada. A local Canadian tech company!

I use it regularly with my firm and it works really well if you got rental properties, a daycare, professional services, branding, or social media type companies. Anytime you have recurring invoices to the same customers, it works extremely well.

I am an accounting partner with Rotessa, which means that my firm and my clients get a discount on their subscription fees. So if you're looking to improve some efficiencies within your company, and if you're looking at maybe what are good payment solutions out there, this is a great solution for that.

I'd be happy to have a discussion on your accounting needs or taxes. Maybe you're looking for a monthly fixed price plan that gives you everything that you need to resolve some of the headaches that you have – because I know that there can be a lot of headaches with bookkeeping and accounting.

That's why I started my firm: to resolve those headaches and to make it easier for you as a business owner.

Accountant & Bookkeeping Partner: Janelle Charriere

Cloud-based bookkeeper, Janelle Charriere, is ready to grow her firm – just one year after opening up shop.

Through working alongside her sister, in her business, Janelle quickly found what she had been looking for in a career. "I've always liked organization and figuring things out," she says.

From Red River College, Janelle has a Business Admin diploma with a major in Accounting. She says she left college "with every intention" to obtain her CPA. But after working in an accounting firm for three years, she was "over that."

Janelle began JCL Strategies in May 2019.

Hiring and Firing the Client

A cloud-based, solopreneur, Janelle calls her own shots and chooses what type of clients she is willing to take on.

12 clients followed her when she left because of the relationships they built together. All her current clients work mostly with trades and are, as Janelle says, "Very easy to deal with."

For Janelle, a good client knows that they don't know what they're doing when it comes to bookkeeping and are willing to let go of control – let someone else do the bookkeeping – because that is not what you, the client, got into business for.

"Working at the accounting firm, you don't say 'no' to anybody. Everybody who walks in the door, wanting bookkeeping, you say 'yes' to – no matter if their books were a disaster or not. The ability to say no to someone because I don't like how they run their business or I don't think we'll be a good fit is a lovely thing."

The idea of hiring and firing clients, while new to the world of bookkeeping and accounting, is a guide for Janelle and how she manages her time and business. When hiring clients, Janelle makes it known that: "if you want things on time, you have to give me things on time."

"It has to be a relationship where we can work together – not against each other and never nagging you."

A word of mouth referral is Janelle's greatest marketing tool. She trusts the clients she loves and assumes the new sign-ups "should have the same mentality" as those lovable clients.

"It can be cool because they [tradespeople] may end up working together. So if one needs something from the other, I can be the in-between and get those files to them. I can make sure that both sides make sense." This ability to work on a project like a team is a great benefit to Janelle and her clients.

Client Requirements

Janelle's clients are also expected to use QuickBooks Online as she knows all the ins, outs, and well, she works for them! In addition to her bookkeeping practice, Janelle trains those switching to QuickBooks Online and offers training services for those who want to try out their hand at bookkeeping.

She says, though, that they soon realize "I want nothing to do with this," and they hire her for their business' bookkeeping needs.

"They know the amount of work that goes in to make their bookkeeping good."

Additionally, anyone who uses JCL will use Rotessa. If you want Janelle to do your books, your payments will be processed by Rotessa with an open authorization.

"Now I don't have to worry about chasing people for money."

In the future, Janelle is hoping to slowly grow her business while keeping the clients she has now. She wants to work with "go-getters" because "I am always trying to find better ways to do things," and doesn't want to work with traditionalists.

To learn more about Janelle and JCL Strategies, visit the website and Facebook page.

Accountant & Bookkeeping Partner: Tanya Hilts

Since 2016 Cloud Bookkeeping Services has used Rotessa to collect payments.

"We adopted the cloud about six years ago," says Tanya, a member of the Rotessa Partnership Program. "We were one of the first 50 in Canada."

Being on the cloud didn't mean not working as a team for Cloud Bookkeeping Services. "We chose to work together even though we had the ability to work remote."

Working through a pandemic

Since the outbreak of COVID-19 in Canada, Tanya and the team have opted to work from home. Tanya admits there has been a little strain in communication since disbanding and working from home, but the tools they were already using has made for an easy-enough transition.

Tanya has now begun to work seven days a week and is taking a proactive approach to her clients' questions about government funding in light of COVID-19. With every new announcement from the government about COVID-19 stimulus money, Tanya posts a summary on social media. She says, "I didn't do it in week one and I got inundated with questions after the Prime Minister's first announcements."

"I think that if I can control the information to the clients, then I can control the clients having to contact me. It's working really well."

Tanya also focuses on strategy with her clients. "I try to reach four or five clients a day to try and figure out who qualifies for what."

For her clients who are non-essential services she says, "I help them focus on thinking outside of the box," so they can continue to operate in a remote world.

Because of Tanya and her team's incredible work ethic and customer service, Cloud Bookkeeping Services has not lost a single client.

"I've actually upsold a few people because they have seen the value we are providing because we are able to go that extra mile."

By looking after her clients' success, Tanya is able to look after her team and business.

A learning curve

Accountants and bookkeepers who were not already working at home didn't have much time to learn the cloud-based ropes. "There has been a steep learning curve," Tanya says.

"For those of us who adopted the cloud earlier, we've been having an easy time through this and then there are still many other people that are still working in physical offices."

Firms who don't have options for working virtually on taxes are struggling. Tanya says, "I think we're going to see a lot of people adopting cloud technology after this."

Cloud-based bookkeeping and accounting tools – like Rotessa – give the flexibility of working from home which, Tanya says, will probably stick around even if we go back to "normal life".

Resources

Tanya provides resources for bookkeepers with her program: Bookkeeper's Bootcamp and on Facebook. She also hosts live discussions on her Bookkeeper's Corner Facebook group on Friday afternoons (which we were very honoured to be a part of one week)!

View this post on Instagram

"We have to get the message out there," Tanya says.

"If we just switch our mindset and focus on customer service and our client, that will help so many people. It's really important for the bookkeeping industry."

At Rotessa, we know that your practice is all about client success. That’s why our partnership program offers added value for accountants and bookkeepers.

With the program, you can expand your reach with unique promotional opportunities, offer discounted pricing to clients and receive top tier support and feedback from Rotessa.

Schedule a demo with Cody or reach out with your questions to our support team.

Relationships and Optimization with 1UP Digital Marketing

If you can believe it, there was a time when Google did not exist. That's how long Phillip Caines, co-founder of 1UP Digital Marketing, has been using and mastering the internet.

"I was always interested in the internet," Phil says. He decoded how these early search engines ranked websites and made websites until he got to the top.

Phil's first top-ranked website may surprise you: "For a time, I had the number one internet listing for Britney Spears of all things!"

That expertise translates into his work today and the competitive space of digital marketing.

Relationships and results

Phil Caines and his team are experts in digital marketing but come to each job with the intention of supplementing and strengthening an organization's marketing needs – not completely taking over.

Since 2013, Phil says, "We, from the very beginning, wanted to be a partner that could be integrated into a marketing department and help take their digital to the next level and actually deliver."

"Not just deliver reports, but actually deliver results."

Being so results-driven has attributed to their strong relationships with their clients.

"We don't have contracts or lock anybody in," says Phil. "We just want to build relationships, build results, and that's been serving us really well for the last seven years."

Another one of 1Up's strengths is being able to keep up with the rapidly changing internet. Phil says the biggest change, that's affected how they do business, is the migration to mobile.

"People are now glued to their mobile devices," he says. "The days of having a full computer in front of you for casual browsing are gone."

The tight-knit team of 5 works one-on-one with their clients to ensure their strategy and content - no matter where it will be viewed - is going to produce results.

"We strive to have a very diverse skill set in each of our account managers. They are not just relationship-focused, but also technically-focused."

"Cutting through the clutter," creates efficient communication within 1UP but – most importantly – also the client.

1Up Digital Marketing and Rotessa

Since 2015 Rotessa has helped 1UP Digital Marketing continue to focus on integration, building relationships, and results.

"We definitely saw the value of the service right away," says Phil.

Neither credit card processors, who were charging too much, and traditional methods of checks fit 1Up's needs.

"To have an almost 'set it and forget it' system that works well with our clients, Rotessa is definitely something that is filling that void."

Sustainable results and practices

1Up's next project is to go green. "We've recently worked out our sustainability policy and have tried to engrain it in every aspect of our business."

Before working remotely was the norm, the team was all commuting in creative and carbon-friendly ways like public transport, walking, or biking.

By also partnering with other companies that have similar goals and takes sustainability seriously, Phil says, "We hope to further the goals of organizations that are trying to do good and really help them get to the next level."

To learn more about 1Up Digital Marketing, visit their website, or follow them on Twitter and Facebook.

Rotessa Building Grand Opening

Our Rotessa Grand Opening was a success!

Over 100 friends and family joined us for an afternoon of wine and cheese to celebrate our new building altogether.

Hitch + Boler Coffee Roasters, our dear friends, provided some really sweet party favours for our guests too! As you can imagine, we are happy to keep all the leftover coffee.

As a team, we take great pride in our building. We loved touring our loved ones through this space that we spend so much time in!

There wasn't much of a formal program – we love to be as relaxed as possible – but did present a video that introduced the team before Greg gave a toast and thanked some key people who were involved in the new building. We won't confirm, or deny, that some happy tears were shed.

Our Grand Opening was a great reminder of the amazing community we are surrounded by.

Now, with all the excitement around the new building dying down, we're getting back to connecting with small business owners like Amy, that need to find a better way to get paid.

A Chance to Dance: Rotessa and Dancers Edge

Since 2012, Dancers Edge dance studio has been giving kids in Saskatchewan the chance to dance.

Amy Bertram purchased Dancers Edge in August of 2019 from a sole proprietor. Dancers Edge was Amy's hometown dance studio growing up in Warman, Saskatchewan.

"I've been here since the beginning," says Amy. She moved her way up from dancing in 24 pieces a season, to becoming an instructor, and finally an office assistant before leaving for university.

"I've had the opportunity to see Dancers Edge grow over the last eight seasons from a small studio, in a small town, with about 50 dancers to 300 dancers and two studio spaces."

Now, as the owner, Amy focuses on more day-to-day tasks like budgeting and marketing but teaches her Adult Barre Fitness and "Parent and Tot" classes. "Totally different ends of the spectrum, but they are both great classes and tons of fun," she says.

Amy is a strong believer that everyone – no matter where they land on that spectrum – should get to dance.

"I am one of those people that believe that dance is for everyone – whether you have $10 in your bank account or you are a millionaire and you want to join every single class that you possibly can. We try really hard to allow the opportunity for every single person to come in and dance."

With their scholarship program, Chance to Dance, dancers who maybe can't afford to pay for classes on their own get that opportunity to earn their spot and dance at a highly competitive level.

Amy, a full-time registered nurse, has a great business mind and has worked hard to grow this "side business". She attributes her business-savvy to her father. Similar to Amy, he has a completely different vocation but owns other businesses.

"He definitely gave me that little spark for sure," she says. "From a young age, he instilled a hard work ethic and a business mind. He is one of the best mentors I have."

Amy admits, "I am more of a registered nurse on the side than a business owner on the side."

When Amy bought the business, the previous owner gave her an overview of Rotessa as parents pay through installments for dance classes. She says, "The website was super easy to use."

"Rotessa has made it very easy for me to send off a form to families who want to pay through installments - it's super quick. They do everything online and then I never have to touch a cheque or input numbers."

"It's probably one of the easiest parts of my job right now."

Since the big leap of growth from 50 to 300 dancers, Amy keeps dreaming of Dancers Edge's next steps: "The next step is to expand our building a bit more. We would like to create more space for our dancers so they can be here and be comfortable spending the evening here while they wait for classes."

For anyone that has an interest in dance, Amy suggests just dipping your toes into one class your first year – or even just a low-commitment, sessional class: "Go for it, start small, and then I guarantee it will be the only year you go small."

For more information and to follow Dancers Edge's growth, visit their website or follow them on Instagram!

Community and online giving for churches in the Yukon

Relationships are a large part of the British Columbia and Yukon District of the Pentecostal Assemblies of Canada (BCYDPAOC).

"The Pentecostal Assemblies of Canada is a network of churches and ministries. Our District Network Office serves the BC and Yukon Region. Our district office team exists as a network hub, to strengthen and extend the ministry of our local churches and credential holders," explains Devan Sylvester, Communications Team lead for the BCYDPAOC.

Based in Langley, BC the team works to serve the churches and their communities in the entire district.

Devan says, "Our District Network team consists of 15 staff, and we serve just over 200 churches representing 32,000 people attending PAOC Churches in BC and the Yukon."

Working in the northern territory of the Yukon also sets apart the BCYDPAOC.

In addition to their other programs and events in British Columbia, Devan says in the Yukon, "We work with indigenous leaders in planting churches, establishing leadership opportunities, raising awareness of cultural language groups."

By building relationships with these communities, Devan says the BCYDPAOC brings value to their communities through "intentional partnerships".

"We desire to be a relationally based mission agency who together share the following values of quality and health of leadership, congregations, intentionality to creative and authentic opportunities to communicate grace and truth within our local communities."

As a not-for-profit, the BCYDPAOC needs to facilitate donations, tithes, and online giving "We have used Rotessa for over five years as a platform for churches, ministries, and persons to process their online bank to bank donations."

Online giving facilitates several regional training seminars and conferences for churches, volunteers, pastors and leaders throughout the year. Devans says, "We also host generational-focused events for students and children in youth and student ministries."

To find out more and to support the BCYDPAOC, visit their website and Instagram.